Being stressed about your finances certainly won't help improve your financial situation.

"People under stress perform differently than when they're not under stress and make all kinds of bad decisions," said Dominique Henderson, a certified financial planner and founder of DJH Capital Management in Cedar Hill, Texas. As a result, their finances can seriously suffer.

Certainly some financial decisions are more nerve-racking than others. Here are some of the most stressful money situations Americans face — and what to do about them.

Buying a home

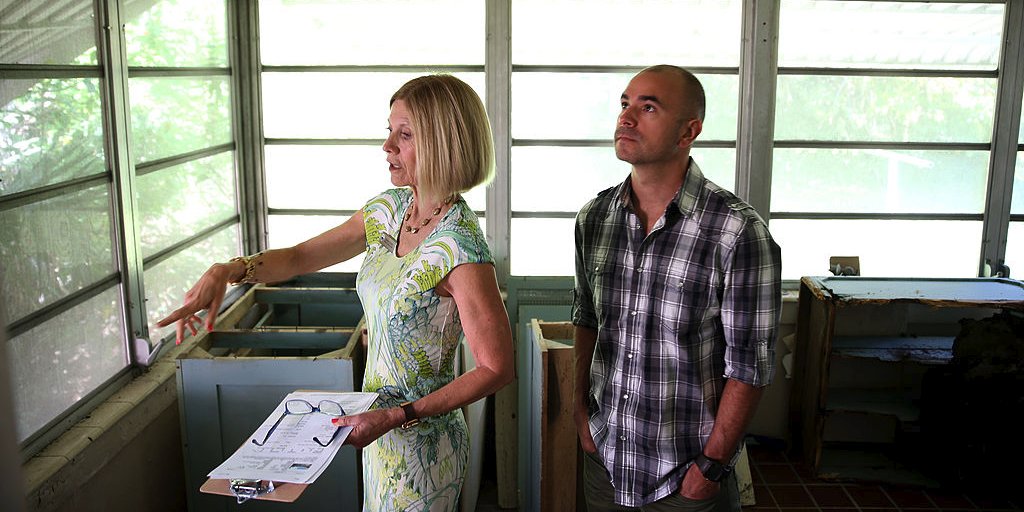

Buying a home can be exciting but incredibly stressful. Online real estate brokerage Owners.com found that 72 percent of potential homebuyers said they expect stress in the homebuying process. Many of the respondents cited the financial aspects of buying a home as their primary worry.

"As one of the largest financial transactions in a person's life, it can be extremely challenging to remove your emotions and approach it with a methodical and rational mind," said Steve Udelson, president of real estate brokerage Owners.com. "This reality is exacerbated even more by the current real estate market, where home prices and interest rates are on the rise, and inventory continues to be low."

Making sure you don't rush is the key to avoiding headaches during the homebuying process. Start by figuring out how much home you can afford based on the amount you have saved for a down payment, and the monthly mortgage amount you can afford to pay without stretching your budget too thin.

Once you've calculated this figure, commit to not exceeding it. Owners.com found that more than half of potential homebuyers were willing to go over their budget by $37,809 on average.

To ensure you don't exceed your budget, Udelson recommends researching the real estate market in your area to understand if the price you're paying for a home is in line with its value. Cut transaction fees with a low-cost brokerage such as Owners.com.

Think critically about how long you will be in the home to determine which mortgage option is best for you. "Thoroughly inspect the home to assess any additional fees before inking the deal," Udelson said.

Knowing when to retire

Perhaps even more worrisome than figuring out how much to save for retirement is trying to decide when to retire. "The anxiety around this question can be overwhelming," Frankle said.

That's because many people don't know if they have enough money to retire. "A bad decision here could mean having to go back to work or relying on the kids," Frankle said. "Both of these outcomes are the last thing anybody wants."

To alleviate the stress, you need to have a plan for exiting the workforce years before you want to retire. "By creating your retirement plan and updating it over the years, you'll have a very good idea of whether or not you are on track, when you can retire and how much you'll have to live on," Frankle said. "Without running a retirement plan, you'll be in the dark, and that spells worry for most people I know."

Consider meeting with a financial planner to develop a plan. You can find a fee-only planner through NAPFA.org, the website of the National Association of Personal Financial Advisors. You can also find a planner who charges by the hour at GarrettPlanning.com, the website of the Garrett Planning Network.

Understanding how to help your aging parents

Figuring out how you can afford to provide support for aging parents can be extremely stressful.

A report by Caring.com found that four in 10 caregivers spend $5,000 or more per year on caregiving expenses. Meanwhile, 18 percent of those caring for a loved one with Alzheimer's disease or dementia will spend $20,000 or more annually. Plus, most caregivers have had to miss work to help family members. That can take a financial toll.

To alleviate some of the stress of this tough financial situation, Henderson recommends having a plan in place well before your parents need care. Talk to your parents about their finances. "Get everyone in (a) room together to discuss basics," he said. Having a conversation well before your parents need care might give you time to help them get insurance coverage for long-term care needs and get all of the proper legal documents — such as a power of attorney — in place so you can step in and take control of their finances, if necessary.

Read the original article on GOBankingRates. Copyright 2017. Follow GOBankingRates on Twitter.