Business Insider

Business Insider

Over the past five years, I've written about money a lot.

A lot.

I don't pretend to be a financial expert or hold any kind of certification, but between writing, editing, and reading hundreds (thousands?) of stories about money, I've picked a few things up.

Chief among them is that the best, most critical first step you can take to improve your finances is to track your spending.

If you think about it for 30 seconds, it makes perfect sense. If you don't know where your money goes today, how are you going to realistically plan where it should go tomorrow? Unless we start writing things down, we're all going to continue lying to ourselves about how much we spend on bagels, anyway.

For a few years, I let LearnVest (where I used to work) track my spending automatically, by connecting my accounts. That was fine, and I recommend it, or a similar service like Mint or You Need a Budget, over doing nothing. But I couldn't get granular enough. I couldn't manipulate the numbers. I couldn't project anything. And I found having 40 category folders in a drop-down list to be tedious.

I started interviewing real people about their budgets for Business Insider, and found myself getting jealous of their spreadsheets. How nimble! How detailed! How customizable!

So I made my own.

Since its creation, I've shared it with a handful of friends, some of whom have shared it with their friends in turn. They've found it useful, so I got to thinking: maybe you would, too.

A few disclaimers before we get to the spreadsheet itself:

• These are not my actual spending numbers. I repeat: These are example numbers. They are not mine. They are arbitrary numbers I chose to demonstrate how the spreadsheet works. I don't want everyone knowing the truth about how much money I spend on chocolate or blowouts. That shame is mine alone.

• The sheet is not that complicated. That's part of its charm. The formulas in the sheet are pretty straightforward: adding, subtracting, dividing. Nothing wild. Consider it a beginner's spreadsheet. If you have impressive Excel skills, go ahead and trick it out.

• It is for tracking your spending, not keeping to a budget. If you want to set up a budget in the traditional sense, imposing spending limits on each category, this sheet will help you establish those limits. However, you'll need to make some of your own additions if you want to track your spending in relation to a budget rather than to get an idea of where your money goes.

• If you want to use it, you'll have to make a copy. It's a plain old Google Sheet, and it's view-only. So make a copy, then enter your numbers. (File > Make a Copy)

Now, to the spreadsheet. Here's how it works:

If you don't want to read about it, skip straight to the spreadsheet »

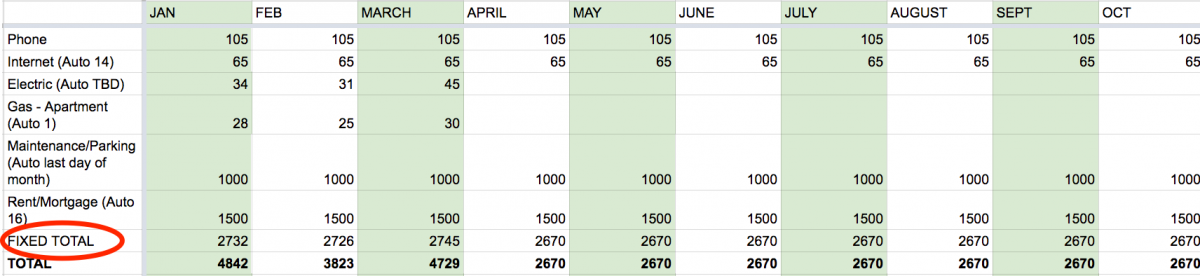

Each column is a month, each tab is a year.

Plus, I added an extra "test" tab, where I copy over the formulas and play with the numbers. What would happen if I saved an extra $500 this month? What about if I didn't buy any chocolate? You'd be surprised at the difference that makes (don't judge).

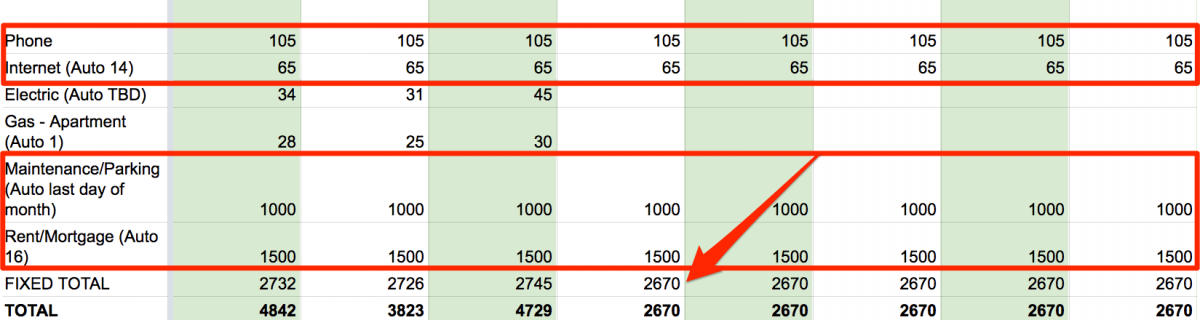

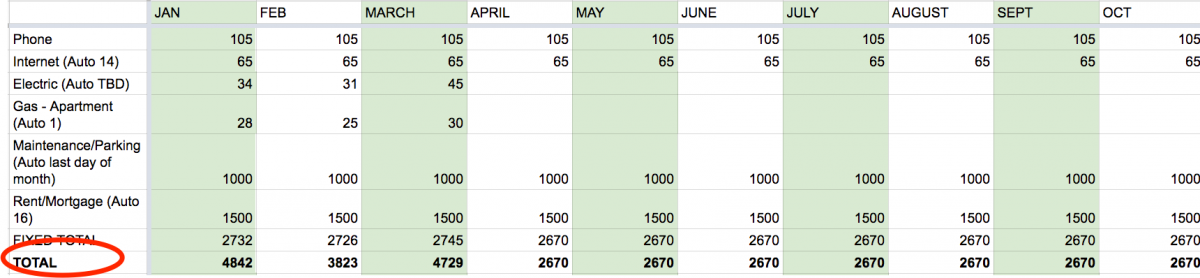

Each January, I plug in my fixed expenses for the entire year.

I know what my mortgage and maintenance payments will be. I know what my phone and internet costs will be.

Plus, plugging in all the numbers in January just means one less field to fill out going forward.

I add those fixed expenses to see what it would cost me to live every month, bottom line.

Planning out my fixed expenses ahead of time, I can see that if I didn't spend a single penny in a month, it would cost me — in the example, anyway — $2,670 to live. That isn't even counting food, or gas, or commuting costs.

If I were to notice that my income was dangerously close to, or even below this number, I would know that my lifestyle was unaffordable and I'd need to make a major change.

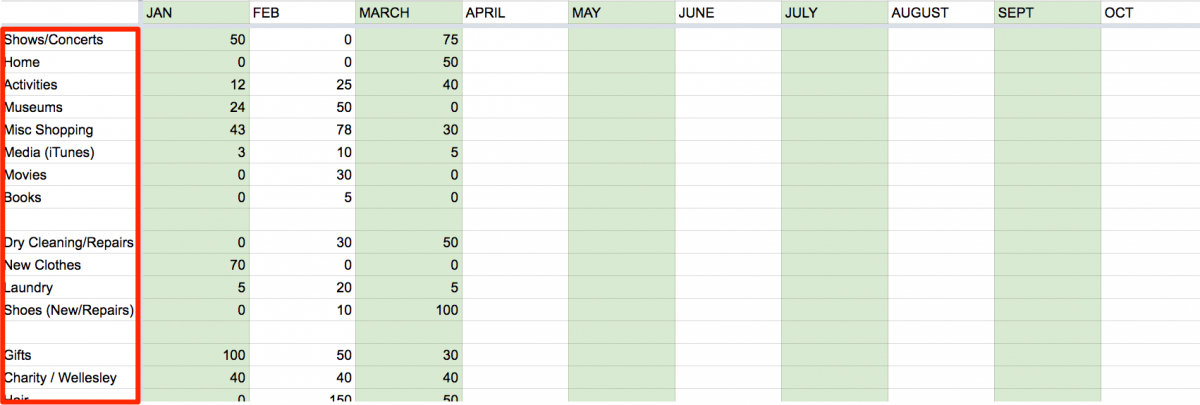

I add categories to the spreadsheet as they become needed.

When I first built the spreadsheet, I thought of as many spending categories as I could. But as time went on, I would notice that I couldn't remember why categories were filling up. How did the "medical" category end up with such a high balance? What about all the money my friend Venmo'd me for drinks? Can I really count chocolate as "food?"

Every time I started getting confused about which expenses went where, I added a new category. For the 2017 sheet (not reflected in the example) I've broken out all of my charitable giving and gift costs.

As I spend, I enter the totals manually. The column to the very far right calculates and shows how much you're spending per month, based on how many months you've filled in data for so far. (Shoutout to Your Money editor Alex Morrell, who upgraded my rudimentary formula.)

You can choose to hide the "Months" column. It's just there for calculation purposes, but I wanted to keep it in there to better show how it all works.

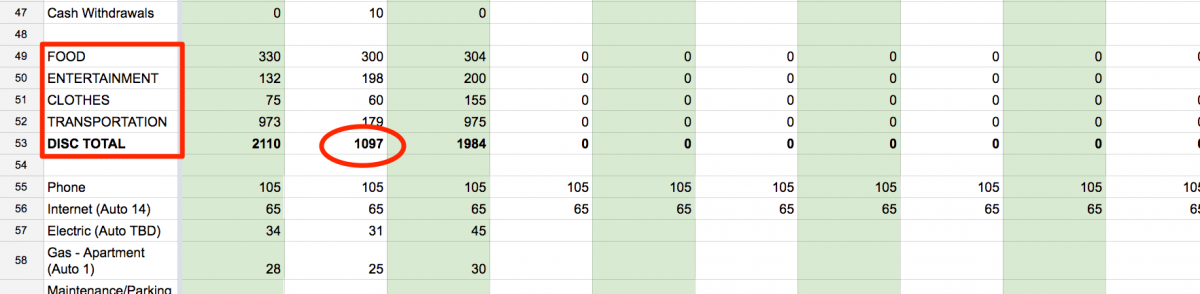

For a broader perspective, all the line-by-line categories are added into a larger groups at the bottom: food, entertainment, clothes, and transportation.

Then, at the bottom of those, they're added into the total amount of discretionary spending for the month.

You could argue that food is necessary, not discretionary, but one of the first things most people overspend on is food — eating out, buying unnecessary groceries, paying for daily coffees. To a degree, it is discretionary, and I'm fine with including it here. You may choose otherwise.

The discretionary total, plus the fixed total, shows me how much I'm spending every month.

That sum is marked "Total."

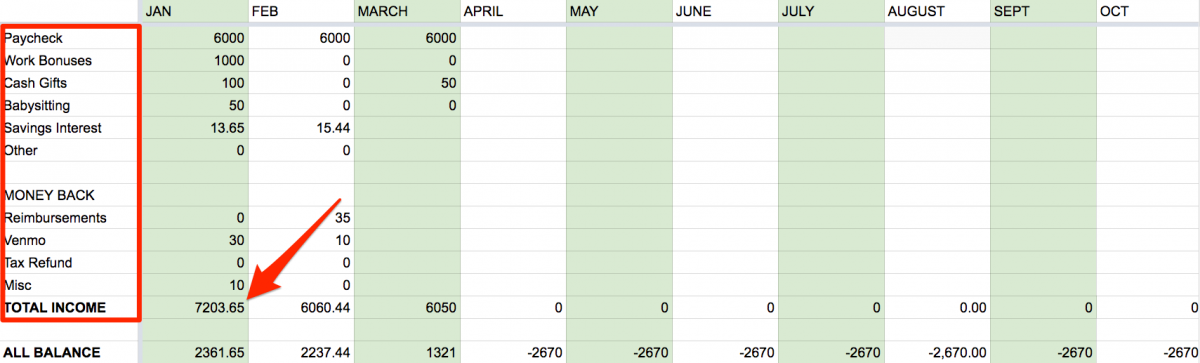

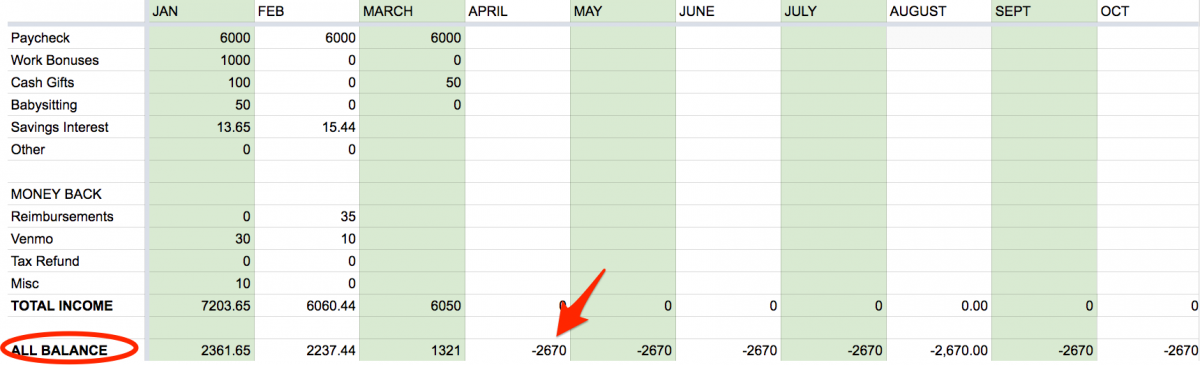

I include money that's been returned to me as part of my total income.

This is a choice I've made, and one that might not work for other people. I'm using "income" here in the very literal sense of the word: money coming in.

If I were to put a group dinner on my credit card to save us all a headache and spot $200, then get a $50 Venmo from my three dining companions, I prefer to put that $150 in money back in its own category, rather than going into the "restaurants" category and subtracting money in increments. If it makes more sense to you to only include your portion of the bill under restaurants, go that route.

I subtract the total from my total income for the month to get the monthly balance: how much money I have left over (or how far in the red I've gone).

You'll notice that in the months where no money has yet been earned, there's a negative balance. That means I've spent more than I've earned — although in this case, that negative balance is thanks to the fixed costs I've projected out in advance. I'm not actually in the red.

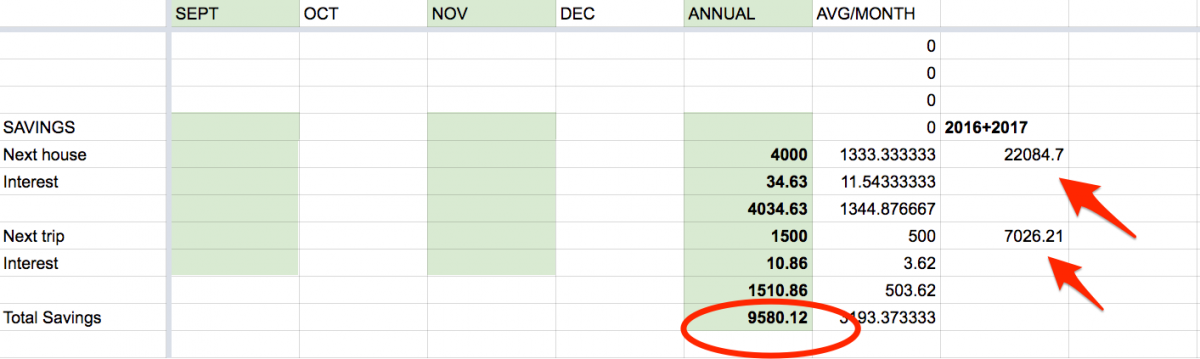

I keep my savings separate.

There is a row for my contributions to each account, and a row for the interest that has been earned. Then, there is a total number for contributions plus interest in each account, and a number for total amount in savings that year in general (in this example, it's $9,580.12).

In the columns to the right, I add those totals to total savings numbers from last year, to keep a running balance of how much savings are in the bank, in all.

If I followed the advice of everyone and automated my savings so each one of the accounts was getting regular monthly deposits without my input, I could project those numbers out for the year. However, I haven't done that for a variety of reasons. You should probably be smarter about this than I am.